May 15 2026

May 15 2026

10 min read

10 min read

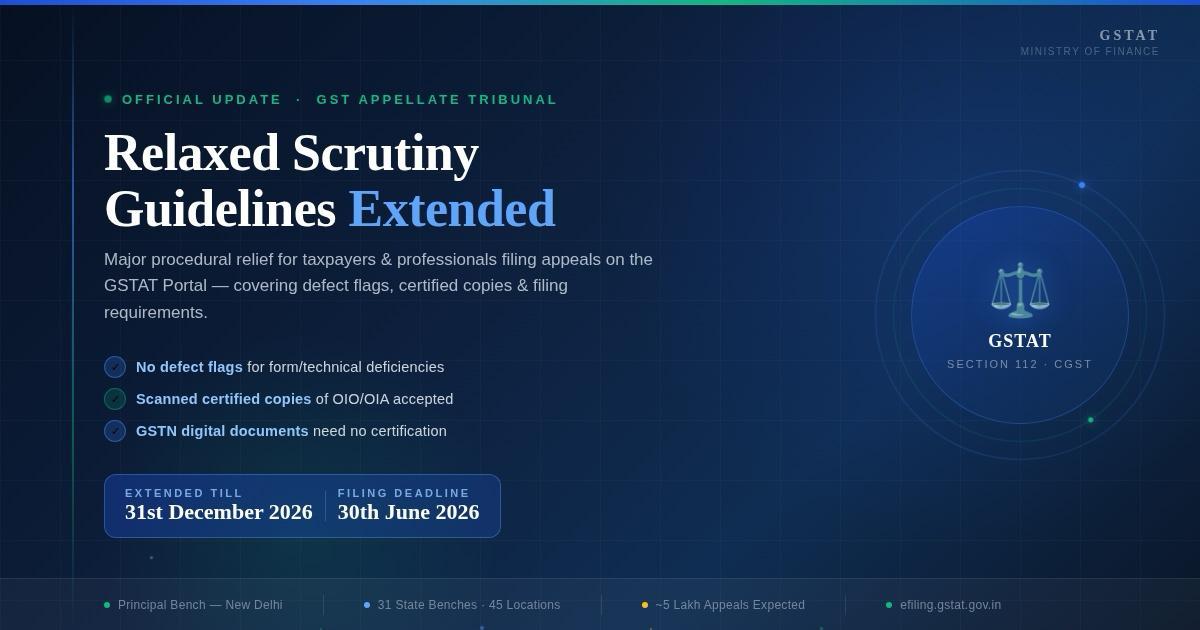

In a significant development providing continued relief to taxpayers, GST professionals, and the legal fraternity, the Goods and Services Tax Appellate Tribunal (GSTAT) has extended its relaxed scrutiny guidelines for the filing of appeals on its e-filing portal till 31st December 2026. This extension carries forward the lenient approach originally introduced through the Office Order dated 20th January 2026, which had initially provided a six-month window of relaxed scrutiny set to expire around July 2026.

The move reflects the GSTAT's recognition that India's appellate ecosystem is still in a transitional phase ? navigating a massive backlog of disputes accumulated over nearly eight years of GST implementation, the challenges of a fully digital filing environment, and the operational ramp-up of 31 State Benches across 45 locations nationwide.

Finance Minister Nirmala Sitharaman formally launched the GST Appellate Tribunal (GSTAT) on 24th September 2025 to expedite resolution of disputes between businesses and the tax department, and ensure fairness in delivering justice. The Tribunal, described by the Finance Minister as a "true symbol of justice for taxpayers," represents India's second-tier appellate forum for GST disputes ? sitting above the First Appellate Authority (Commissioner Appeals) but below the High Court.

The GSTAT formally commenced its first phase of adjudicatory operations on 16th February 2026, with the Principal Bench at New Delhi and several State Benches ? including Cuttack and Delhi ? becoming functional for hearing cases. Around 4.83 lakh cases pending before the appellate authority are expected to be filed before GSTAT, with approximately 2 lakh appeals anticipated by the June 30, 2026 deadline.

The Principal Bench issued an Office Order dated 20th January 2026 exercising powers under Rule 123 of the GSTAT (Procedure) Rules, 2025, directing all bench registries to adopt a lenient approach while scrutinising appeal filings for six months from the order's issuance.

Under the Office Order No. GSTAT/Pr.Bench/Portal/125/25-26|2711-15 dated 20th January 2026, the following key directions were issued:

The original 6-month window was set to expire around 20th July 2026. The extension of this relaxed scrutiny regime to 31st December 2026 is driven by the following compelling ground realities:

Earlier, the GSTAT filing system restricted users from proceeding to subsequent stages of appeal filing unless payment details were first updated on the portal. This technical restriction created practical difficulties for taxpayers and professionals, particularly in situations where preparation of appeal documents was completed but payment formalities were pending. While improvements have been made progressively, digital bottlenecks and portal issues continue to affect the filing experience for many appellants across the country.

With nearly 5 lakh cases expected to be filed before GSTAT, the ecosystem needed more time to stabilise. Many appellants ? particularly those dealing with orders from 2017 to 2022 ? face genuine difficulty in procuring old physical documents and having them certified in time. For these cases, the lenient scrutiny regime provides a meaningful safety net to prevent technical rejections.

Not all 31 State Benches across 45 locations became fully operational simultaneously. The rollout of state benches faced delays beyond initial deadlines as necessary staff and infrastructure were not fully ready in some centres. Taxpayers filing before benches still ramping up operationally deserved the protection of lenient scrutiny during their initial admission process.

All appeals before GSTAT against orders of the appellate or revisional authority in APL-04 communicated on or after 1st April 2026 must be filed within three months of the order being communicated. Extending lenient scrutiny to December 2026 ensures that filings made under this new wave of orders also benefit from procedural flexibility during the admission phase, creating a level playing field for all appellants.

The most business-friendly aspect of the extended relaxed scrutiny regime is the moratorium on raising "form defects." Under the extended guidelines:

One of the most practically significant reliefs under the extended guidelines relates to the submission of certified copies of impugned orders. The GSTAT instructions issued vide F. No. GSTAT/Pr. Bench/Portal/125/2025-26/3868 dated March 10, 2026 clarify:

In cases where a higher court has granted exemption from payment of court fees or pre-deposit, scrutiny officers should not raise any defect flags regarding such requirements. This is a crucial safeguard for taxpayers who have ongoing High Court proceedings or who have received stay orders from superior courts. Such appellants must furnish proof of the relevant judicial orders, and no defect shall be raised against them at the scrutiny stage.

While the extension relaxes scrutiny of form, certain substantive requirements remain firmly in place. Appeals filed in Form APL-05 must mandatorily include:

The appellant taxpayer must upload an authorization in favour of the tax professional or a Vakalatnama executed in the name of an advocate, wherever representation is involved. GSTAT has also mandated that only one verification and a digital signature of the appellant will be required for filing the appeal electronically, which reduces the procedural burden while maintaining integrity of filings.

For appeals filed by the Revenue Department under sub-section (3) of Section 112, the GSTAT has specified the documents that must accompany the application: Show Cause Notice, Order-in-Original, Order-in-Appeal, Statement of Facts, Grounds of Appeal, and the opinion of the Commissioner directing the concerned officer to file the application. Departmental appeals do not require pre-deposit or court fees, and these provisions remain unchanged under the extended framework.

In a significant operational improvement, the GSTAT portal has now been enhanced to allow appellants to upload documents and complete checklist compliance independently of fee payment status. Earlier, the system restricted users from proceeding to subsequent stages unless payment details were first updated, creating practical difficulties particularly where document preparation was complete but payment formalities were pending.

This portal upgrade, combined with the extended relaxed scrutiny, creates a more forgiving and user-friendly appeal environment ? a combination that tax practitioners and bar associations had been strongly advocating for through formal representations including those by the Marwar GST Bar Association.

The extension of relaxed scrutiny to December 2026 must be understood alongside the broader filing deadlines:

The June 30, 2026 filing deadline remains firm and non-extendable. However, if you filed your appeal before June 30 and face scrutiny defects, the extended relaxed regime until December 31, 2026 gives you additional time for curative filings without risking rejection on technical grounds. This is particularly valuable for MSMEs and businesses dealing with orders from 2017-2022 where documentary challenges are acute.

Appeals filed within three months of order communication will benefit from the extended lenient scrutiny regime through December 2026, reducing the risk of rejection on formal grounds during the admission stage. This gives practitioners the breathing room to file promptly while refining documentation.

The extension validates the strategic advice to file appeals promptly, even if documentation is imperfect. The lenient regime provides a meaningful opportunity to cure minor deficiencies without losing the right of appeal. Importantly, filing after the lenient scrutiny period ends means full scrutiny standards apply ? every formatting imperfection becomes a potential defect that could delay admission.

The extension of relaxed scrutiny guidelines till 31st December 2026 is a mature and pragmatic decision by GSTAT ? one that balances the imperative of access to justice with the practical realities of a new tribunal system finding its feet. It sends a clear message: the GSTAT is committed to resolving GST disputes on their merits, not on technicalities of form.

For India's taxpaying community ? particularly MSMEs, mid-size businesses, and multi-state enterprises facing years-old disputes ? this extension provides breathing room, operational clarity, and confidence in the appellate system. For the broader GST ecosystem, it signals that India's indirect tax dispute resolution architecture is maturing, with fairness and efficiency as its twin pillars.

The window of opportunity is still open. File now, file right, and let the merits of your case speak for themselves.

Important Note: The June 30, 2026 filing deadline for legacy pre-April 2026 orders remains firm and absolute. The relaxed scrutiny extension to December 2026 governs the post-filing scrutiny and admission process ? it does not extend the limitation period for filing. Taxpayers must ensure their appeals are filed within the applicable statutory timeframes. This article is for informational purposes only and does not constitute legal advice. Consult a qualified GST professional for case-specific guidance.

Comments (0)